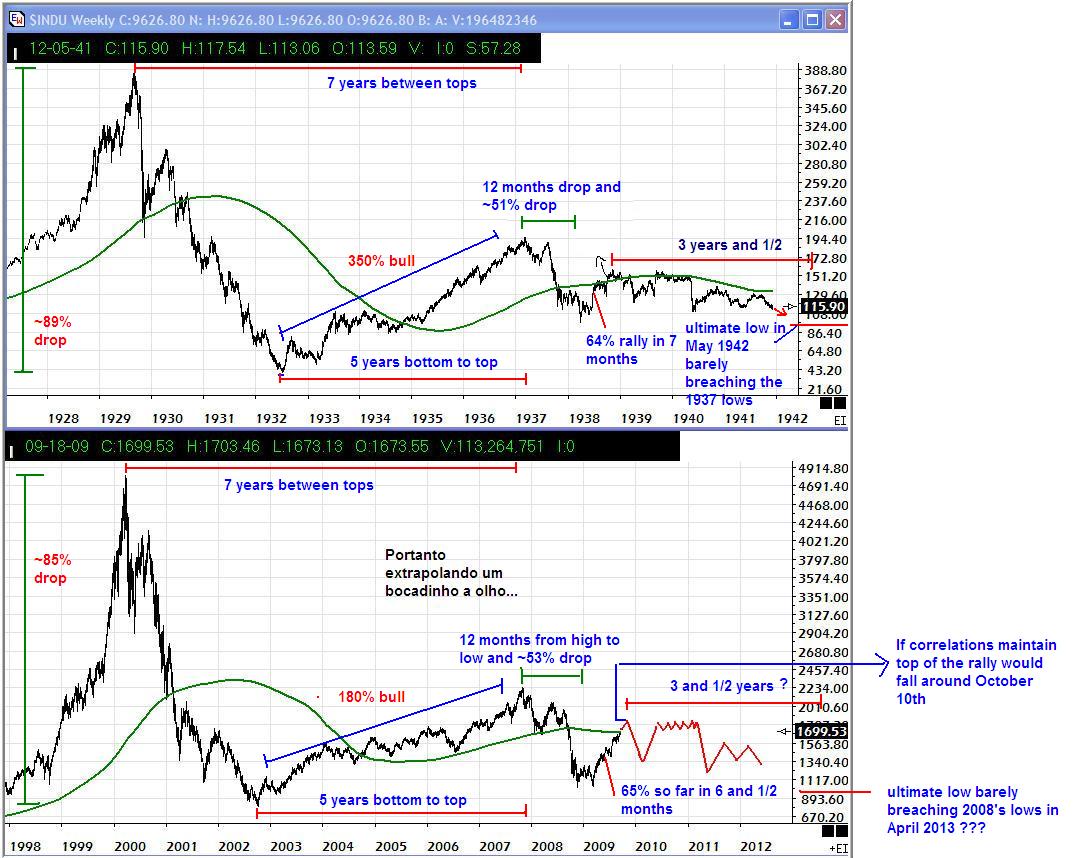

It is remarkable how much the 1930s DOW chart resembles the NASDAQ 2000s chart. The boom and bust nature of the roaring 20s and the technology boom of the 80s and 90s illustrates the fact that human psychology remains at least one constant in the stock market.

From their inception, both the early DOW and NASDAQ experienced years of uninterrupted growth before making their final parabolic moves and then subsequent crashes. The DOW took 12 years to fully "correct" before resuming a long term uptrend that began in 1942. We are 10 years into the NASDAQ's long term period of price consolidation. The real question is how much more time is required for the NASDAQ to fully consolidate and are we headed lower first?

One striking difference between these two charts is the magnitute of their second bull run after their massive crashes. After correcting 89% from its peak, the DOW broke out of a 3 year base pattern and moved up 380%. The DOW subsequently came back to test the 100 point level in 1938 and one final time in 1942 after which a long term uptrend resumed. The NASDAQ, however, moved up a mere 180% after its crash only to break support and retest its crash lows in 2009.

What does this mean? After a significant 380% rebound, it took two retests of the 1935 break out level support at ~100 to wash out all weak investors and the DOW to finally break out in 1942 and never look back. With respect to the NASDAQ, all of the weak holders were washed out in 2008 by a near retest of the 2002 crash lows. A second retest of the 2002 crash lows is unlikely. Support is more likely to hold near 2000 points or slightly below this level. The chart above suggests the NASDAQ will lack direction and drift to the old lows. I don't think so but anything is possible.

So perhaps it takes a year or two more before the NASDAQ defines itself as the true market leader once again. What's more important is the long term uptrend that will follow. In approximately 60 years, the DOW surged 1000% or two exponential steps. It stood at 100 points during the 1940s, moved up by one exponential step to 1000 points during the 1970s, and subsequently moved by another exponential step to 10 000 points by the year 2000. Each exponential move required approximately 20 years to complete, followed by a 10 period of price consolidation.

The NASDAQ currently sits at ~2000 points. By 2020 the NASDAQ should make one exponential step to 20 000 points and then enter a period of price consolitation during the 2030s. The uptrend will then resume in approximately 2040 with the NASDAQ reaching a remarkable 200 000 points, a second exponential step, by 2060 give or take a few years.

What's more interesting is where the other indicies will be given these time frames. Following the same trend, the S&P 500 and DOW shoud reach 10 000 and 100 000 points respectively by 2030. The following exponential step would bring the S&P 500 to 10 000 points and the DOW to a whopping 1 million points by the year 2060.

Sounds silly right? Imagine, how many people would have believed you if in 1942 with the Great Depression fresh in the entire world's mind, you made a prediction that the DOW which then stood at a mere 100 points, would reach 10 000 points by the year 2000?

This is the nature of exponential growth.